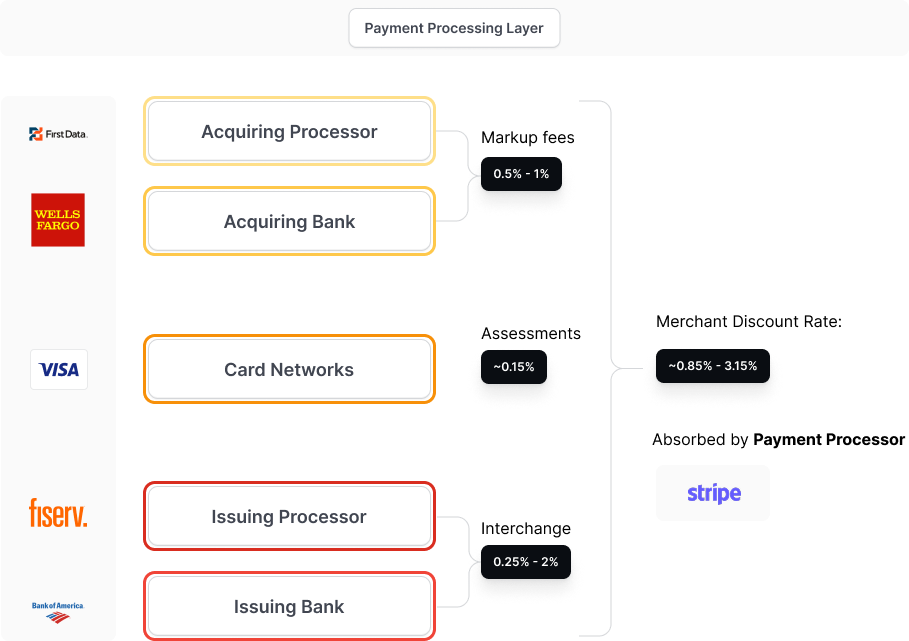

What are 'interchange rates'

Interchange rates are fees charged on credit card and debit card transactions by the card networks (Visa, MasterCard, Discover, American Express). Interchange fees compensate the issuing bank and card networks for providing and managing payment cards, cover transaction risk and fraud, and help fund rewards programs and network infrastructure. Interchange fees typically show up as a percent rate (%x.xx) and a fixed fee ($0.xx), and often include additional 'assessment fees' that are applied based on the 'scenario' of the transaction that are typically also a percent rate (%x.xx) and a fixed fee ($0.xx).

How many different interchange rates are there?

There are thousands of different types of interchange rates, but the main categories that create the variations in fees are typically one of the following categories:

1. Card Brand. Like Visa or American Express?

2. Card Type. Like a Debit Card, Credit Card, or Corporate Rewards?

3. Bank Type. Like Regulated or Unregulated (over $10b in assets or under)?

4. Merchant Category. Like Nonprofit or Utilities?

5. Transaction Type. Like the card was charged in person swiped or Online (card-not-present)?

6. Transaction Size. Like how large is the transaction?

7. Transaction Region. Like purchaser location, currency of initiated transaction, merchant location, currency of merchant settlement?

Each of these categories combine to create unique combinations for each of the card brands, who set specific rates and fees. These show up as an interchange or assessment fee.

How often are interchange rates set?

The card brands publish new rates every year, although the rates and fees don't always change.

How do credit card rewards affect cost?

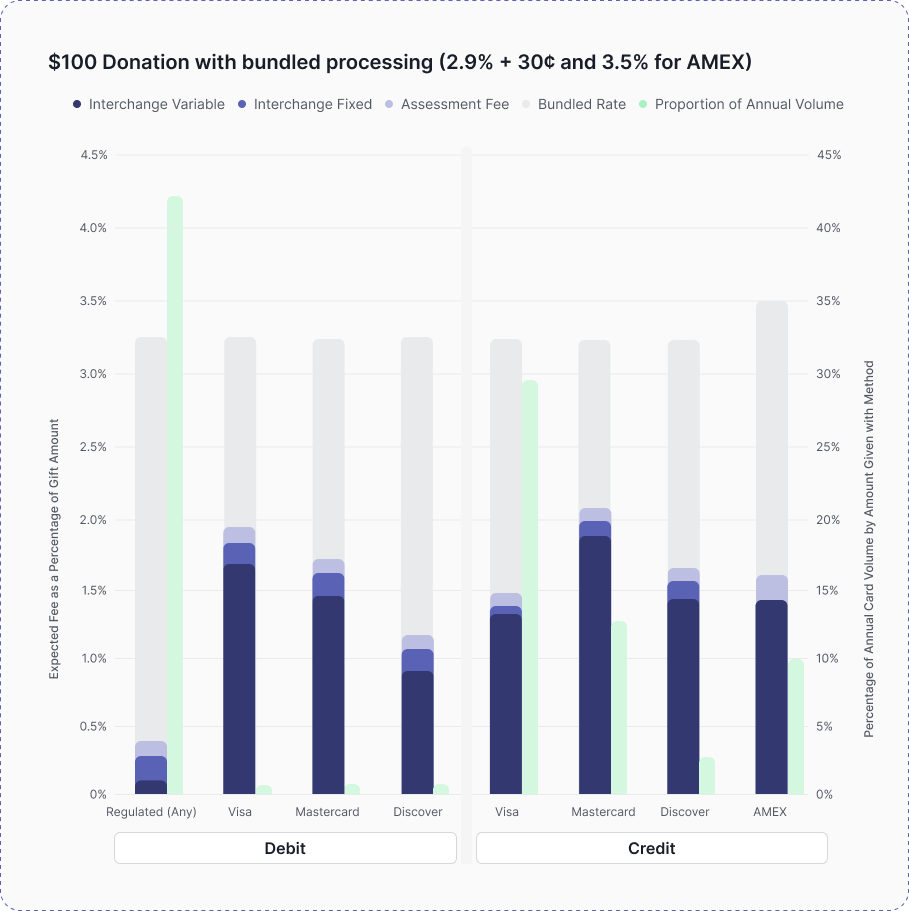

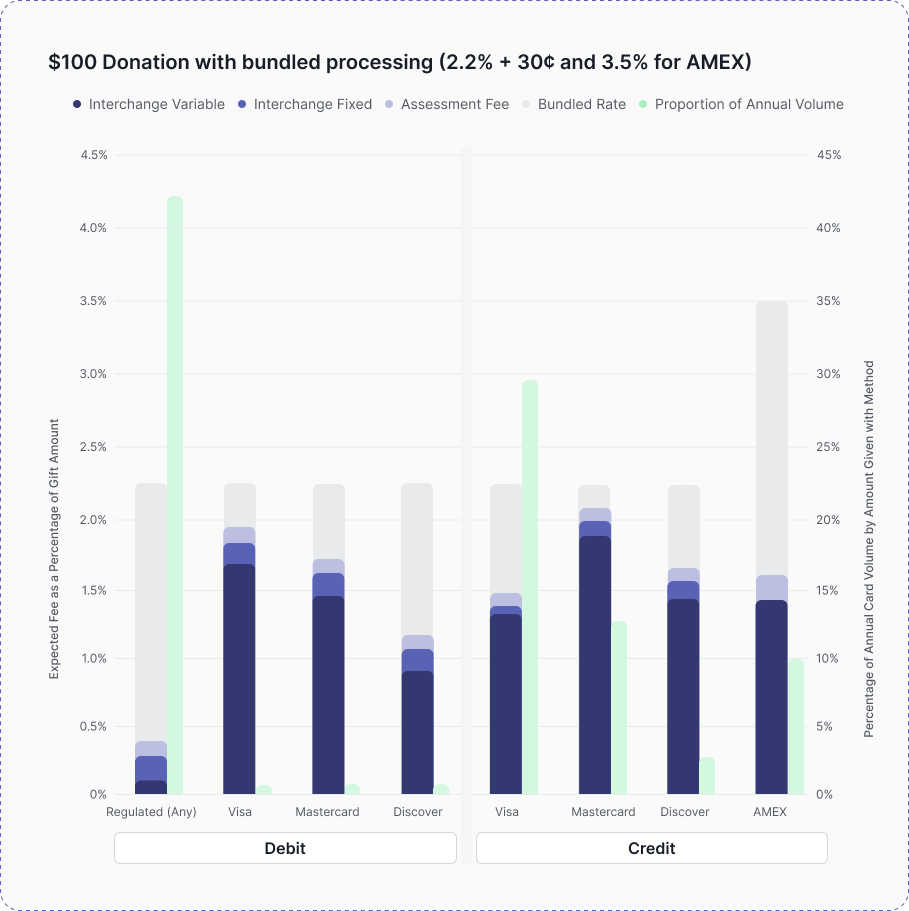

Typically, the cards with the biggest rewards are the most expensive. For example, American Express charges the highest interchange rates because the purchaser gets, typically, the best credit card rewards when using it. A debit card, which has the least rewards because it's a direct charge to the purchasers bank account and does not include any benefits or points, has the least expensive interchange rates when working with a regulated bank (a bank with over $10 billion in assets under management).

How does industry affect cost?

The industries with the largest risk (as in the highest likelihood of fraud) have the most costly rates for doing business. A merchant selling alcohol or luxury items like jewelry online naturally attract more fraud than a merchant that accepts payments for water utilities via billing. A fraudster is less likely to pay their utility bill and more likely to purchase something they want or can re-sell.

When are the interchange rates charged?

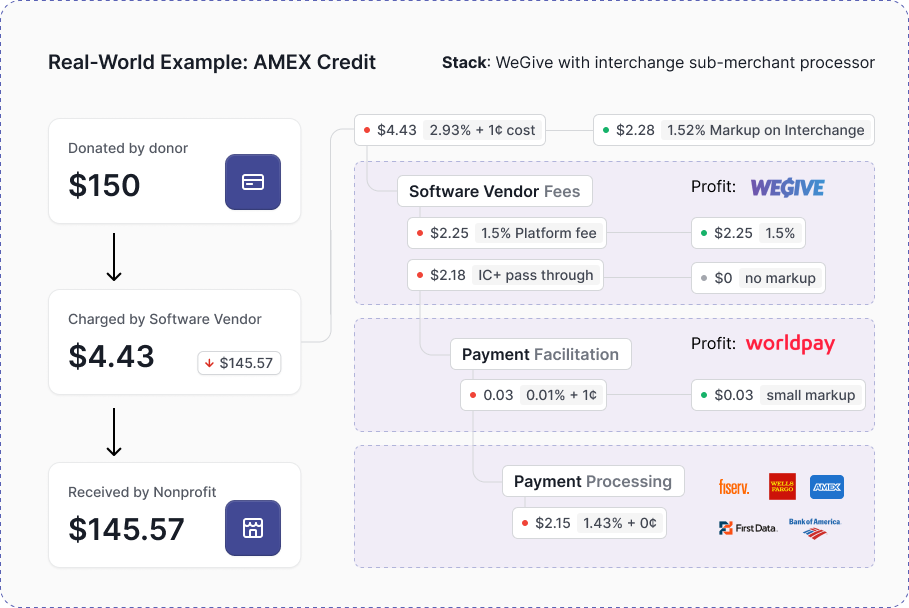

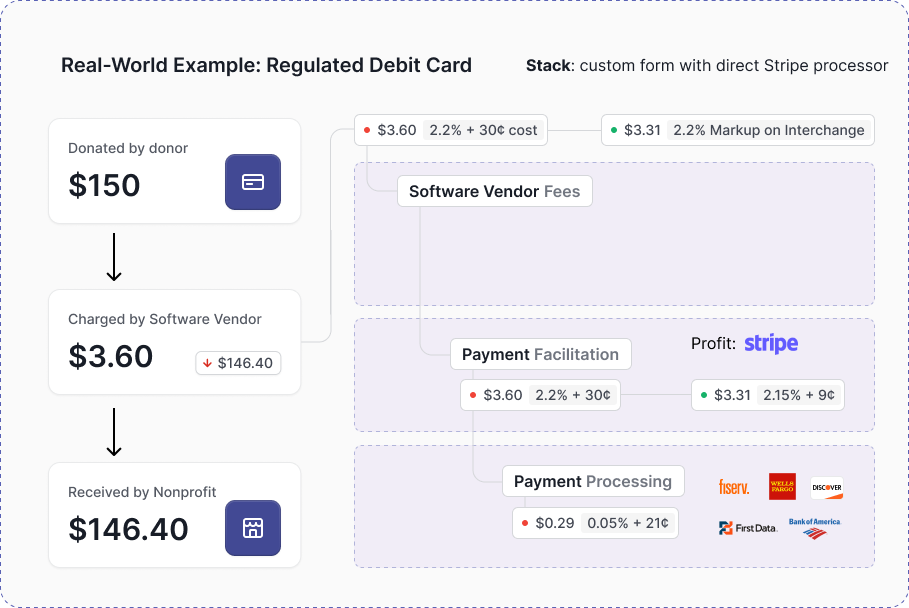

Merchants (the nonprofit organization) pays for the payment processing to the payment processor at the moment the transaction occurs. The payment processor pays the interchange fees and assessment fees over the coming days to the purchaser (the donor's) bank and/or card network as the assessment fees are applied during the payment processing and settlement.